A Family of 3 Living in New York City on $500K

How parents of a 19-month-old approach savings for college and beyond in one of the country’s most expensive cities.

A lot of families wonder whether they should open a 529 college savings account for their new baby. It can be almost impossible to imagine what the world will be like when our tiny babies are ready to go to college. Will they even want to go to college? Will college even be a thing or will robots run the world? And aren’t there other goals we should be saving for like our own retirement?

In our most recent installment of Baby Balance Sheet, we’re featuring a family in New York City who asked many of these questions. Ultimately, they decided to open the 529 for their young daughter—they share their thought process below.

Every family has to make their own decision when it comes to whether they want (and can) invest in a 529. To help you navigate this and other money tools, we have lots of helpful guides so you can understand how these accounts work.

Read on to see how this family of three are juggling competing financial priorities: saving for college, saving for a new home, and paying for daycare.

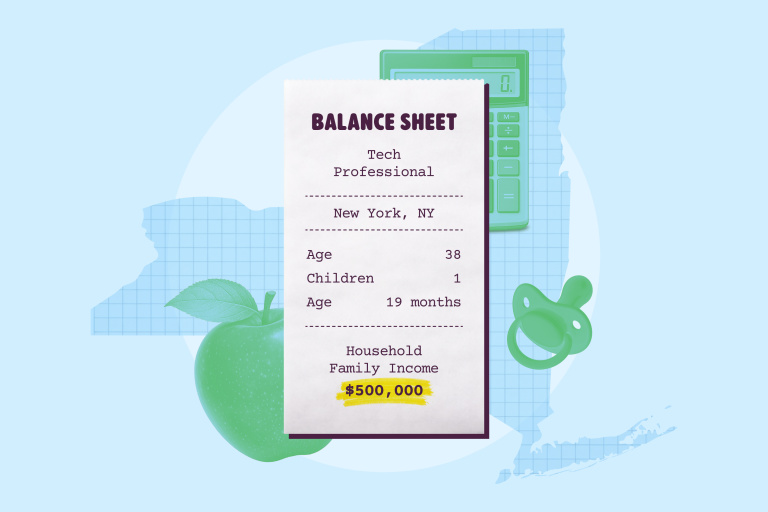

About me: I am a tech professional. I love to ski, do pilates, and I recently picked up road cycling! I live with my husband and daughter in Manhattan.

Age of parents: I’m 38, and my husband is 37.

Age of baby: 19 months

Where do you live? New York City

What is your family household income? $500,000

Did you have a savings goal before your baby arrived or are you working toward one now? We save $500 per paycheck into a joint high-yield savings account that is meant for home and child expenses. Additionally, I save $100 per month in a 529 account, and $2,000 per month goes into a brokerage account that’s earmarked for medium- and longer-term expenses—like buying a new house and sending our daughter to college.

What kinds of financial tools (or tricks!) are you using to help reach your savings goals? We use automatic transfers into our joint account. We don’t do anything fancy though.

Are you setting up any savings accounts for your baby—like a 529, custodial account or something else? If yes, what kind of account(s) are you using? Originally, I didn’t feel the need to set up a 529 account. I am unsure if traditional education will be the same once my daughter is at the age where she would potentially go to private school (12 to 14 years from now) or college (17 to 21 years from now). I’ve since decided to set up one and make small monthly contributions because I see the value of the long-term tax benefits. Also if she doesn’t use it for education she could convert that account into a Roth IRA. My in-laws have set up a custodial account for my daughter and put in a significant contribution each year—up to the gift-tax maximum—which is very generous. It’s not likely we’ll use the money in the custodial account for education. Ideally, she’ll be able to use it when she’s an adult for a big expense like buying a house.

If you’re setting up a savings account for your baby, are you hoping friends or family might contribute to it too? As mentioned above, my in-laws have their own custodial account for my daughter that they’re contributing to. My parents are not familiar with or interested in exploring financial instruments for their granddaughter, but they do give us small monetary gifts on occasion, which we usually put into our joint account.

When it comes to money, what part of having a baby (or raising a kid) feels most stressful? I had paid leave, which was amazing. I am definitely trying to stay employed in a role with paid leave in case we decide to have a second child. Daycare is a serious strain on our finances. We spend more than $4,000 a month. We live in a neighborhood in Manhattan where child care is very expensive—we’re not even using the most expensive option. But my husband and I both work full-time, and we really like our daughter’s daycare. We know she’s safe and well taken care of. I used to have much more flexibility with my finances. I was able to spend more money on myself, going out to eat or buying fun clothes. Now I have to be very deliberate about my spending. We are unsure if we will have a second child because of the costs of child care. We are exploring the idea of private school for my daughter, but that would be out of the question if we had a second child. My in-laws are very pro private school and are encouraging us to take steps toward getting our daughter into one of the “feeder” preschools for the private schools in our neighborhood. Those options would be more expensive and give us less child care coverage so my husband and I are not eager to go that route.

Are you receiving (or will you receive) any family help for paying for baby expenses? My parents will sometimes buy us an outfit or two for my daughter, but outside of that we don’t get any help from them. My daughter does have a custodial account set up by my in-laws, which she will be able to access when she is of-age. Right now, the three of us are living in a one-bedroom apartment that we converted into a two-bedroom. It’s pretty small, and I’d love for my husband’s parents to help support us with money for a down payment on a bigger place, ideally in a different neighborhood.

Can you share how much you spent on your baby/children in the last month?

Daycare: $4,474.60

Waterwipes: $15.19

Mustela baby cleaning water: $20.16 Johnson’s Baby Fluffy Bubbles bubble bath: $4.78

Owala tumbler: $12.99

Ten Little Splash sandals and charms: $53.60

Uncle Bubbles Mini bubble blower: $11.99 (My daughter loves bubbles but can’t blow them with a traditional wand just yet. This is perfect to help her get the joy of bubbles while she builds her strength.)

Little Kicks soccer class: $40 (drop-in)

Kids clothing: $49.90 BJs Wholesale (including monthly diapers and weekly milk): $627.31 Local grocery store and farmer’s market run: $229

Laundry card: $35 (we have laundry in our building and we pay for our runs via credit card)

Cryofreezing bill: $115 (I froze my eggs when I was 30, and I’ve been paying for their rent ever since.)

How much do you discuss the cost of raising a baby with your partner?

I’d say I’m more on top of our finances than my husband is, though we do talk about money-related things all the time. I make quite a bit more money than he does, and we keep our finances separate. Each of us takes on a few different expenses that we “own.” I pay for our daughter’s daycare, and he covers expenses like insurance (home and auto), etc.

Right now, our biggest concern is trying to figure out if we can afford to buy a bigger home somewhere else in New York City. We’ve got a Covid-era mortgage rate, which keeps our housing costs very low. It’s like golden handcuffs! It’s hard not to give up.

My husband’s parents have a lot of wealth, and I’m trying to convince my husband to talk to them about giving us some of his inheritance early so we can buy a better home now. I have a really big fear that we’re going to be priced out of New York. But he has to have that conversation with his parents—not me—and he has to figure out the right time to do it.

We have been sharing the financial details of all kinds of different families in our series Baby Balance Sheet. Read about a family of 3 in Tulsa, Oklahoma living of $43,000 and a family of 4 in Indiana living of $220,000.